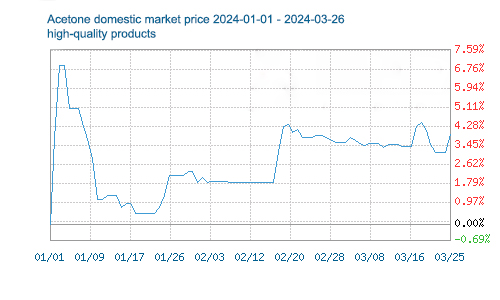

In March, the domestic acetone market fluctuated slightly, with the main end-user purchasing power being limited, and the fluctuation range was 0.31%.

The acetone market adjusted weakly in the first half of the month, with little room for market fluctuations. At the beginning of the month, the supply of imported goods was sufficient, and port inventories increased rapidly. However, the listed prices at factories remained stable, and traders’ mentality was still supportive. Downstream demand is mainly rigid, procurement is mediocre, and both supply and demand are weak. The market fluctuations are relatively small. In the first half of the month, the fluctuation space of major mainstream markets is mostly 20-50RMB/ton.

The acetone market was mixed in the second half of the month. Port inventories were insufficient that week, and the supply side in East China was expected to be tight. Traders had a positive attitude, and the offers in major mainstream markets quickly pushed up. However, there was obvious resistance to high prices due to limited downstream follow-up. After the 20th, as the supply side became loose again, the market fell by 80-100RMB/ton. Although the amplitude was not large, it was the largest fluctuation in the month. It is expected to fluctuate in a range until the end of the month.

From the supply side, as port inventories increased at the beginning of the month, the supply in East China was sufficient, while petrochemical companies stabilized their offers and listed prices remained stable, making the market offer prices relatively stable. However, at the beginning of the month, Zhejiang Petrochemical’s Phase I 650,000 tons/year phenolic and ketone plant resumed operations. The operating rate of social enterprises remained at 70-80%. Manufacturers shipped goods as planned, and there were many negative factors on the supply side.

From a cost perspective, the domestic pure benzene market fluctuated little in March. It first declined and then rose in the first half of the month. The market was basically stable in the second half of the month. Compared with the previous period, the current pure benzene market is still within the high range. Because it provides strong support to the downstream acetone market from a cost perspective, phenolic ketone companies are still losing money.

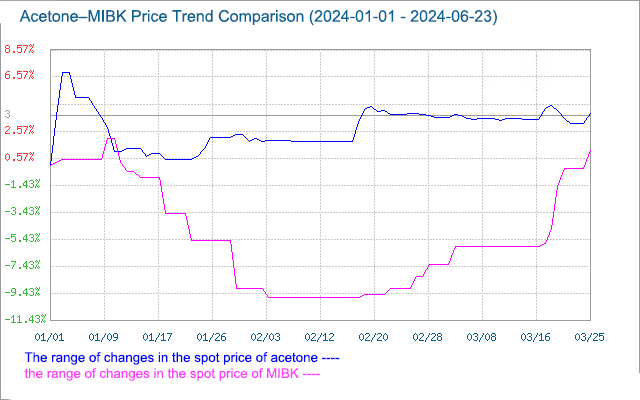

From a downstream perspective, the domestic MIBK market rose steadily after stabilizing in March, while the bisphenol A market fell slightly in March due to poor demand.

At the end of March, acetone was approaching settlement, the contract was exhausted, and the market focused on maintaining stable operation. In the later period, there will be fewer bullish factors, general purchase sentiment on the demand side, limited real transaction volume, current cost side is still supported, factory prices will not fluctuate much, and we will pay attention to the weekly port inventory situation in the later period.

Post time: Mar-26-2024