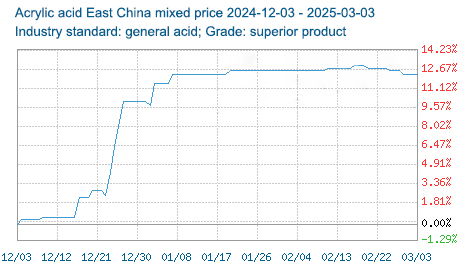

1. Price Trend

Fluctuating downward

The mainstream transaction price has recently fluctuated in the range of 8,000-8,500 yuan/ton, down about 10%-15% from the high at the beginning of the year, and the market transaction center of gravity has gradually moved downward.

Low-end sources (especially in East China) have fallen below 8,000 yuan/ton, and some manufacturers have made concessions for shipments, exacerbating the bearish sentiment in the market.

Regional differentiation

Prices in the main sales areas such as East China and South China have fallen significantly due to high supply pressure and weak demand; North China is relatively resistant to price drops due to local rigid demand.

2. Core factors affecting prices

Demand continues to be weak

Downstream industries such as coatings and textiles: Affected by the downturn in the real estate market and the reduction in export orders, the operating rate is only maintained at 50-70%, and purchases are mainly small orders for rigid needs.

Adhesive industry: Demand in the packaging field has seasonally rebounded, but the increase is limited, and it is difficult to reverse the overall weak demand.

Supply pressure increases

The industry’s operating rate has rebounded to more than 75% (such as the load increase of large factories such as Satellite Chemicals and Yangba), and the commissioning of some new production capacity (such as a new 100,000-ton unit in Shandong), the market spot is loose. Social inventory increased by about 15% month-on-month, and manufacturers have a stronger willingness to reduce prices and destock.

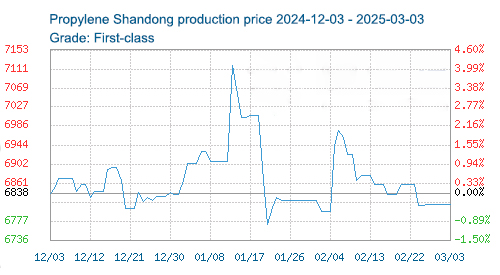

Limited cost support

The price of raw material propylene fluctuates with crude oil. At present, the arrival price of propylene in East China is about 6,500-6,800 yuan/ton, which has weak support for acrylic acid costs. The acrylic acid-propylene price gap has narrowed to 1,200-1,500 yuan/ton, and some companies are close to the break-even line, but have not yet triggered large-scale production cuts.

3.Future price trend prediction

Short-term (1-2 months): Weakness continues, bottom oscillation

Demand is unlikely to improve significantly, coupled with loose supply, prices may continue to fall to the range of 7,800-8,200 yuan/ton. If the sharp rebound in crude oil prices drives up propylene costs, or downstream concentrated inventory replenishment, the decline may be temporarily stopped, but the rebound space is limited.

Medium-term (3-6 months): Marginal improvement, but pressure remains

Potential positives: The implementation of domestic policies to stabilize growth (such as infrastructure and consumption stimulus) may drive the recovery of demand for coatings and textiles; overseas economic recovery may boost export orders.

Risk points: The concentrated release of new production capacity (expected to exceed 500,000 tons in the second half of the year) may suppress the price recovery.

4.Operational suggestions

Traders: Prioritize digesting existing inventory and avoid hoarding; pay attention to low-priced sources and replenish small orders at low prices.

Downstream enterprises: Purchase on demand, forward orders within 3 months to reduce the risk of cost fluctuations.

Production enterprises: flexibly adjust loads according to profits, strengthen binding with downstream long-term customers, and reduce spot sales pressure.

In summary, the acrylic acid market is still in a downward cycle dominated by “weak demand + high supply” in the short term, and prices may further bottom out. In the medium and long term, it is necessary to observe the effect of policy stimulus and the rhythm of overseas demand recovery. If the supply and demand structure improves, prices are expected to stabilize and rebound around the end of the year. It is recommended that market participants maintain a low inventory strategy and focus on cost fluctuations and downstream replenishment signals.

Post time: Mar-04-2025