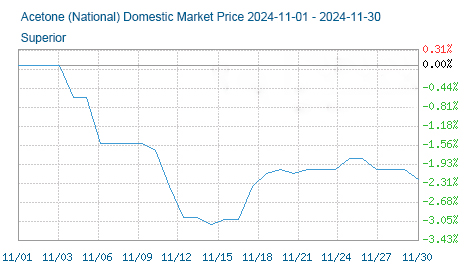

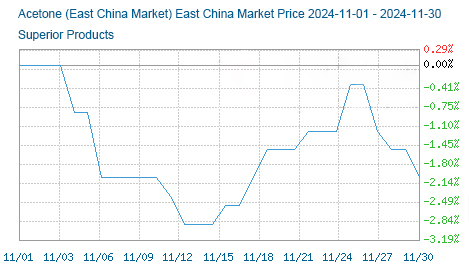

The acetone market fell slightly in November. According to analysis, the national acetone market fell from the average quotation on November 1 to 2.24% on November 30. As for the acetone market in East China, the quotation in East China rose from November 1 to 2.04% on November 30.

Average price trend of acetone in the national market

Acetone price trend chart in East China market

In the first half of the month, the first phase of Lihua Yiweiyuan and the first phase of Huizhou Zhongxin phenol ketone units were shut down for maintenance, and the overall operating rate of domestic phenol ketone units declined. Dongying Fuyu’s 100,000 tons/year acetone unit was put into trial operation and sales began one after another, which aggravated the market’s wait-and-see sentiment. Traders began to arrange shipments according to market conditions, sporadic profit concessions appeared, and the market fell significantly.

In the second half of the month, with the arrival of port cargoes for replenishment, port inventories increased rapidly, acetone continued to fall, and then downstream factories tendered for replenishment, the atmosphere improved, traders’ intention to sell at a low price weakened, and there was no lack of price support for shipments. In the second half of the month, Sinopec Mitsui and Qingdao Bay phenol ketone units were shut down for maintenance one after another, the operating rate of domestic phenol ketone units declined, spot resources were slightly tight, terminal factories sporadically entered the market to replenish stocks, and the atmosphere improved.

At the end of the month, the trading atmosphere cooled down, traders quoted prices according to market conditions, terminal factories purchased on demand, and the actual trading volume was limited. In the absence of sufficient transactions, the market was deadlocked and the transaction was flat.

From the supply perspective, as of the end of the month, the inventory at Jiangyin Port was 28,500 tons, including 26,000 tons at Huaxi and 2,500 tons at Hengyang.

In terms of equipment: Jilin Petrochemical’s equipment was shut down for maintenance from March 4, and is expected to last about a year; Changchun Chemical’s equipment was shut down for maintenance from October 10 to November 21; Lihua Yiweiyuan’s first phase equipment was shut down for maintenance from November 1 to 7; Sinopec Mitsui’s equipment was shut down for maintenance from November 19 to 27; Huizhou Zhongxin’s first phase equipment was shut down for maintenance from November 1 to 30; Qingdao Bay’s equipment was shut down for maintenance from November 18 to 24.

From the demand side, the operating rate of downstream isopropanol and MIBK units has increased, the operating load of bisphenol A and MMA is low, and the demand for acetone has not changed much.

It is expected that the market will fluctuate within a narrow range in December. From the cost point of view, crude oil performance is weak, and the pull of pure benzene is weakened. The units have been restarted one after another, and the overall operating load of domestic units has increased to more than 80%. The import contract sources from Saudi Arabia and Thailand have arrived as scheduled, and the import volume is expected to be at the level of 30,000 tons. It is expected that the acetone market will fluctuate within a narrow range in December, and the actual trading volume needs to be followed up.

Post time: Dec-02-2024